Mallorca in European Comparison: Second-Home Locations Face Off

Anyone considering a second home in the Mediterranean in 2026 will almost inevitably end up choosing between three options: Mallorca, the Côte d'Azur or Tuscany. The Mallorca second-home comparison is worthwhile because, at first glance, the three locations seem similar – Mediterranean climate, international buyer base, premium price level – but on closer inspection differ considerably: in price dynamics, tourist demand, inheritance and wealth tax, and connectivity from the DACH region. This guide classifies the available market and tax data from official sources, compares Mallorca with its two major European competitor locations, and shows you what you should really pay attention to when deciding on a location – beyond glossy brochures.

Unsure whether Mallorca, the Côte d'Azur or Tuscany is the better fit for your situation?

- 📩 Submit a personal enquiry — individual assessment of budget, region and usage profile

- Regional price comparison in Mallorca

- Download the free 2026 property market report (PDF) — all figures and regional profiles in detail

Market status 2026: Where Mallorca stands in Europe

By 2026, the Balearics are no longer a rebound market but a supply-constrained, internationally capitalised location. House prices in the fourth quarter of 2025 stood at plus 13.4 percent year-on-year, just above the Spanish average of 12.9 percent. Four different public sources measure price levels using different methodologies – which is why the following figures should be read side by side, not added together.

| Indicator | Source | Period | Value |

|---|---|---|---|

| Average sale price (all residential properties) | Spanish Association of Notaries | February 2026 | 3,880 EUR/m² |

| Existing properties Balearics | Spanish Land Registry | Q4 2025 | 4,127 EUR/m² |

| New-build properties Balearics | Spanish Land Registry | Q4 2025 | 3,995 EUR/m² |

| Existing properties Palma city | Spanish Land Registry | Q4 2025 | 4,086 EUR/m² |

| Total aggregate Balearics | mallorca.com Aggregation | Q4 2025 | €4,101/m² |

In addition, asking-price analyses from property portals (Source: Engel & Völkers, as of June 2026) show a continuous upward movement over several years – useful for gauging medium-term momentum, even though asking prices cannot methodologically be equated with transaction prices.

| Year | Avg €/m² Houses | Avg €/m² Apartments |

|---|---|---|

| 2023 | 3.932 | 4.009 |

| 2024 | 4.113 | 4.537 |

| 2025 | 4.489 | 5.095 |

| 2026 | 4.704 | 5.384 |

Note: Price acceleration slowed noticeably in 2026 compared to previous years (houses +4.8% instead of +9.2% the year before), but remains well above the long-term average. For a purchase decision, the specific Region.

Price levels head-to-head: Mallorca, Côte d'Azur, Tuscany

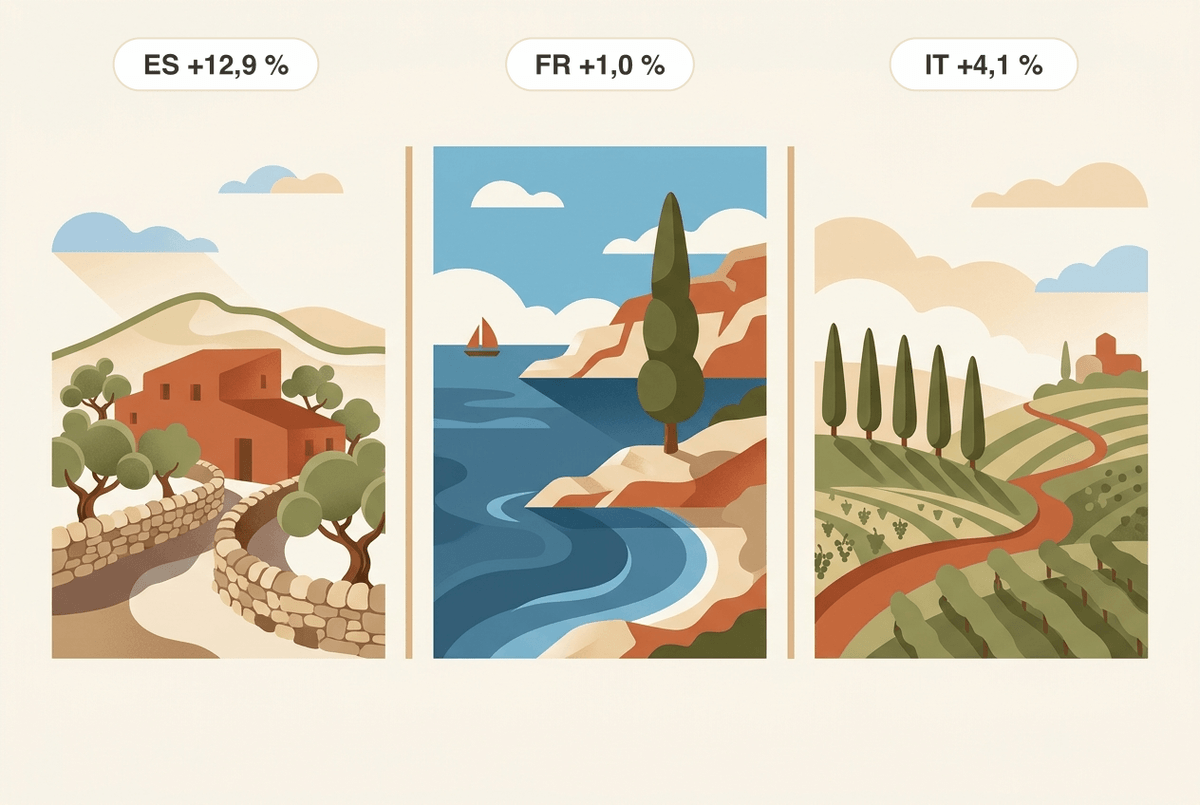

The clearest European comparison can be drawn using the year-on-year house price index – a momentum indicator, not a ranking of absolute price levels. Important to know: according to market data from commercial providers, the absolute price level in premium locations on the Côte d'Azur or in Tuscany remains significantly above Mallorca's level. What does differ markedly, however, is the growth dynamic of recent quarters.

| Quarter | Spain YoY | France YoY | Italy YoY |

|---|---|---|---|

| Q1 2024 | +6.4% | −4.8% | +1.6% |

| Q4 2024 | +11.4% | −1.9% | +4.4% |

| Q2 2025 | +12.8% | +0.7% | +3.9% |

| Q4 2025 | +12.9% | +1.0 % | +4.1 % |

Spain, and with it the Balearics, shows price growth clearly above that of France and Italy. France even saw a real decline again in 2024, before the market stabilised in 2025.

A second, underestimated point of comparison is tourist demand – it is the structural foundation of any rental or resale prospect.

| Region | Hotel arrivals 2019 | Hotel arrivals 2024 | Change |

|---|---|---|---|

| Balearic Islands | 10.58 million | 12.40 million | +17.2 % |

| Tuscany | 9.42 million | 8.98 million | −4.7 % |

| Provence-Alpes-Côte d'Azur | 11.11 million (2016) | n/a | limited data availability since 2017 |

Tuscany remains below pre-pandemic levels in 2024, while the Balearics have not only completed their recovery path but expanded it structurally. For the Côte d'Azur, no comparable regional figures have been available since 2017 – the comparison here is only of limited reliability and should therefore not be over-interpreted.

Eight regions, one market: Where in Mallorca the comparison pays off

Before comparing Mallorca as a whole to another destination, you should know: the island is not a homogeneous market. Eight regions with very different investor profiles are spread across the island's 53 municipalities.

| Region | Population | Profile | Investor type |

|---|---|---|---|

| Palma (city + Marratxí) | 475.208 | Urban economy, urban premium | Core, highest liquidity |

| Southwest (Calvià, Andratx) | 68.979 | International premium locations | Lifestyle core |

| North (Pollença, Alcúdia) | 80.017 | Bays, tourism focus | Yield, highest licence density |

| Northwest/Tramuntana | 30.509 | UNESCO World Heritage, heritage | Legacy, low turnover |

| Northeast (Cala Ratjada, Artà) | 34.181 | Tourist clusters | Yield + lifestyle |

| East (Manacor, Felanitx) | 77.530 | Finca stock | Value-add |

| South (Santanyí, Llucmajor) | 71.302 | Newer building stock | Lifestyle core |

| Island centre (Pla) | 122.544 | Wine corridor, traditional | Value-add, lowest price per m² |

This spread is one of the reasons why a blanket "Mallorca price" says little in a European comparison: the southwest, with its international premium segment, tends to be closer in price to many locations on the Côte d'Azur, while the island centre, with its lower price per m², is more reminiscent of rural regions of Tuscany – though a direct price comparison would need to be checked on a case-by-case basis. You'll find a more detailed breakdown in the guide on the Regions in price comparison.

Buyer structure: who really invests in a second home in Mallorca

The share of foreign buyers in the Balearics stood at 31.47 percent in the fourth quarter of 2025 – the highest of all Spanish provinces, compared with a Spanish average of around 14 percent. The DACH region together forms by far the largest buyer group among international purchasers; within DACH, Germany is clearly ahead of Switzerland and Austria.

| Metric | Value | Source/Period |

|---|---|---|

| Share of foreign buyers Balearics | 31,5 % | Land Registry, Q4 2025 |

| Foreign buyer share Spain overall | 14,0 % | Land Registry, Q4 2025 |

| Mortgage originations per month Balearics | approx. 1,250 | Land Registry, Jan/Feb 2026 |

| Foreclosures Q4 2025 | 45 | Land Registry (vs. 105 in Q4 2024) |

Note: Local Spanish buyers finance predominantly via mortgages, while buyers from DACH, Scandinavia and the UK appear significantly more often with a high cash component. This makes bidding processes in premium locations structurally faster – anyone relying on financing should arrange a mortgage as a non-resident early on.

Tax framework in comparison

In recent years, the Balearics have introduced regional tax rules that set the location apart from other European second-home destinations. This overview is market observation, not individual tax advice.

| Regulation | Balearics 2026 | Note |

|---|---|---|

| Inheritance tax for close relatives | significantly reduced since 2023 | Groups I/II (spouse, children, parents) |

| Lifetime gifts | Reduction expanded since 2025 | analogous to the inheritance rule |

| Wealth tax allowance | €3 million per person | Spain standard: €700,000 |

| Beckham Law (IRPF special regime) | 24% flat tax on Spanish earned income | up to six years, tied to relocation of residence |

Note: A pure property purchase does not automatically trigger tax residency in Spain nor the Beckham Law regime. Anyone who spends more than 183 days per calendar year in Spain is generally considered tax resident (residente fiscal) and is taxed on their worldwide income via IRPF; anyone below that threshold is considered a non-resident and is subject to IRNR. Details on wealth tax can be found in the guide Wealth tax when buying property, on inheritance in the guide Inheritance & Gift Tax Balearics.

The specific tax burden depends on the degree of kinship, asset structure, tax residency and the double taxation agreement with your home country – in any case, you should clarify this individually with a property purchase lawyer and a tax advisor before deciding on a structure.

Holiday letting: licences as a location factor

Anyone wanting to rent out a second home, at least partially, must hold an ETV licence (holiday rental licence) on Mallorca. Since April 2025 these have essentially been halted for flats – new licences are practically no longer being issued, and existing licences are only transferable under certain conditions.

| Region | Licences | Pool ratio among existing properties |

|---|---|---|

| North | 5.326 | 51 % |

| South | 2.800 | 53 % |

| East | 2.209 | 59 % |

| Island centre (Pla) | 2.174 | 48 % |

| Northeast | 1.533 | 49 % |

| Northwest/Tramuntana | 1.162 | 28 % |

| Southwest | 1.026 | 37 % |

| Palma | 804 | 50 % |

In total, Mallorca counted 17,034 active licences in May 2026. The North dominates in volume with around 31 percent of all island licences, while the Southwest is more restrained in numbers but shows the highest concentration of professional marketing. A licence is a prerequisite for legal rental – not a promise of returns. Details on transferability can be found in the guide Transferring an ETV licence, and for specific yield calculations in the guide Mallorca Yield 2026.

Infrastructure comparison: connectivity, schools, healthcare

A second home thrives on accessibility and year-round usability – and here Mallorca has made a structural leap in 2026. Palma Airport recorded around 33.81 million passenger movements in 2025, making it the third-largest in Spain and the fourteenth-largest in Europe. By summer 2026, three premium long-haul routes will be added: the expanded Newark flight, a new connection to Montreal (from 17 June 2026) and a new connection to Abu Dhabi (from 12 June 2026).

| Country of origin | Direct connections summer 2026 |

|---|---|

| Germany | 30+ routes |

| Switzerland | 6+ routes |

| Austria | 5+ routes |

| USA (expanded) / Canada (new) / UAE (new) | 1 premium long-haul route each |

For DACH buyers, the dense daily frequency from Frankfurt, Munich, Zurich and Vienna means a weekend accessibility that hardly any other island in the Mediterranean offers. In addition, Mallorca has eleven internationally recognised schools (seven of which follow the British curriculum, one German school abroad – the Eurocampus Deutsche Schule in Palma-Son Vida), as well as around 750 to 900 private hospital beds across two major clinic groups (Quirónsalud, Juaneda). Between 150 and 200 German-speaking doctors practise on the island.

Financing 2026: interest rates and affordability compared

The Euribor, the reference rate for variable mortgages in Spain, has risen noticeably since summer 2025.

| Period | 1-year Euribor |

|---|---|

| July 2025 | 2,079 % |

| February 2026 | 2,221 % |

| March 2026 | 2,565 % |

| April 2026 | 2,747 % |

The Spanish reference rate IRPH stood at 2.84 percent in March 2026 – the effective bank margin therefore remains moderate by historical comparison. For local buyers, however, affordability is becoming noticeably tighter:

| Indicator | Balearics Q4 2025 |

|---|---|

| Monthly mortgage payment (median) | EUR 1,298.30 |

| Total monthly debt burden | EUR 2,675 |

| Debt-to-income ratio | 55 % |

Please note: A debt-to-income ratio of 55 percent is well above the historically accepted level of around 35 percent. This affects primarily local, credit-financed buyers – capital-strong international buyers with a high equity ratio are far less affected by this development. More on this in the guide Mortgage for non-residents.

2007 in the rear-view mirror: is Mallorca overheated today?

Price growth of plus 12.9 percent year-on-year has only been recorded in six quarters in Spain over the last twenty years – between Q1 2006 and Q4 2007, immediately before the crash of minus 16.1 percent through to Q3 2012. A valid point of comparison, but the structural conditions today differ significantly.

| Structural factor | 2007 | 2025/26 |

|---|---|---|

| Share of foreign buyers, Balearics | under 20% | 31,5 % |

| Lending standards | very soft, high LTV ratios | regulated, under banking supervision |

| New-build volume Spain | around 760,000 homes/year | around 100,000–120,000 homes/year |

| 1-year Euribor | over 4 % | around 2.75 % (April 2026) |

This is not an all-clear signal, but a structural observation: the same price acceleration, but a fundamentally different buyer and lending mix. Anyone buying today should be aware of this difference, but should still approach financing with due caution – see also the guide Mallorca Property Market 2026.

Most common mistakes when comparing locations

- Comparing average prices without regional context. An island-wide average price says little about the southwest or the island's interior – within Mallorca, the price range between regions is considerable, so a comparison with other locations should always be region-specific.

- Confusing YoY growth with absolute price levels. Mallorca is growing faster than the Côte d'Azur, but in absolute terms its premium locations remain below it in price level.

- Planning to rent out without checking the licence. Since the freeze on issuing new holiday-rental licences in April 2025, an existing, transferable ETV licence can no longer be taken for granted.

- Equating tax residency with a second home. Buying a property does not automatically make you a tax resident – only the 183-day rule or the centre of your economic interests determines that.

- Ignoring interest rate developments. With a debt-to-income ratio of 55 percent in the local market, a solid equity ratio is more important today than it was two years ago.

What comes next? Your roadmap to a second home

- Clarify budget and usage profile – personal use, rental, or a mixed model determine the choice of region.

- Narrow down the region – based on the eight Mallorca profiles and in comparison with your reference location (Côte d'Azur, Tuscany).

- Preliminary tax check – clarify residency status, inheritance and wealth tax implications with a Spanish tax advisor.

- Explore financing options – Work out equity ratio and interest-rate fixing in light of the increased Euribor.

- Clarify the licence question if letting is planned – have transferability checked before the purchase contract.

- Reservation contract and notary appointment – see Reservierungsvertrag Spanien and Notar Spanien.

Checklist: Location decision for a second home in Mallorca

- Price level of the desired region compared against Grundbuchamt data rather than just asking prices

- Foreign-buyer share and bidding situation in the target region researched

- Tax-residency status (183-day rule) clarified for your personal situation

- Inheritance and wealth tax rules of the Balearics discussed with a tax adviser

- ETV licence situation in the target region and transferability checked, if letting is planned

- Financing structure calculated under the current Euribor level

- School and healthcare infrastructure of the region compared against your own requirements

- Comparable offers obtained from Côte d'Azur or Tuscany to put Mallorca into realistic perspective

FAQ

Conclusion

The Mallorca second-home comparison shows that the island's prices are growing faster in 2026 than those of the Côte d'Azur and Tuscany, yet remain below them in absolute premium price level. What structurally sets Mallorca apart from the other two locations is the combination of the highest foreign-buyer share of all Spanish provinces, a regionally reduced inheritance and wealth tax, a long-haul network significantly expanded in 2026, and a year-round infrastructure of schools and private clinics. At the same time, the market is no sure thing: the ETV licence freeze since April 2025, a 55 percent debt-to-income ratio among local buyers, and the memory of 2007 call for careful due diligence. Anyone who weighs these factors against their personal situation – use, budget, tax residency – makes a well-founded rather than an emotion-driven location decision.

Official sources

- Instituto Nacional de Estadística (INE), house price index and statistics – https://www.ine.es

- Banco de España, Euribor and lending standards – https://www.bde.es

- Colegio de Registradores de España, land registry statistics – https://www.registradores.org

- Consejo General del Notariado, sale price statistics – https://www.notariado.org

- Agencia Estatal de Administración Tributaria (AEAT) – https://www.agenciatributaria.es

- Agència Tributària de les Illes Balears (ATIB) – https://www.atib.es

- Govern de les Illes Balears – https://www.caib.es

- Aeropuertos Españoles y Navegación Aérea (AENA), passenger statistics – https://www.aena.es

- Eurostat, European house price and tourism statistics – https://ec.europa.eu/eurostat

- Boletín Oficial del Estado (BOE) – https://www.boe.es